Three M's of Homeownership

Among the many reasons people have to own home, they include having a place of their own, to raise a family and to share with friends. Additional benefits include security, investment, peace, pride and enjoyment.

|

Together with the benefits come the responsibility to take care of the home for its livability and viability as a sound decision. A homeowner’s concerns can be broken down into three areas.

The maintenance on the property is something that every homeowner deals with. Changing filters are easy to handle yourself. Other things might require a skilled professional but identifying the “right” one can be challenging.

Minimizing expenses can reduce the cost of living in the home. It’s good to recognize when a repair is appropriate compared to a replacement. Reputable and reasonable service providers are key to keeping expense low.

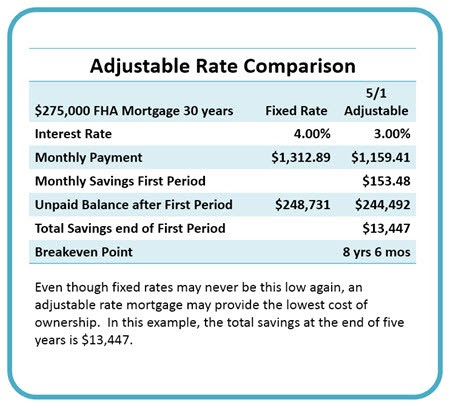

Managing debt and risk becomes the financial side of the effort. Taking advantage of low interest rates or shorter terms for refinancing, making additional principal contributions are just a few ways to manage debt. Home warranty programs and homeowner insurance tips can reduce risk.

We sincerely want to be a resource for you not only when you buy or sell but all of the years in between. It is actually the reason we send this newsletter to you.

Information courtesy of Montgomery AL Real Estate Experts Sandra Nickel Hat Team.

Reasons not to downsize:

Reasons not to downsize:  Mow your grass before you leave for your vacation. I would suggest that you set the mower on the shortest cut you can get so that you don’t have to worry about it growing up while you are gone. If you are going to be gone for an extended period of time you may want to arrange to have a family member mow your yard at least once while you are gone. Mowing your yard before vacation makes it look like you are still at home and therefore may keep away potential intruders.

Mow your grass before you leave for your vacation. I would suggest that you set the mower on the shortest cut you can get so that you don’t have to worry about it growing up while you are gone. If you are going to be gone for an extended period of time you may want to arrange to have a family member mow your yard at least once while you are gone. Mowing your yard before vacation makes it look like you are still at home and therefore may keep away potential intruders.

Reminiscing is easier when scrolling through pictures to remind you of people and times. One of the least heard regrets is that we should have taken more pictures.

Reminiscing is easier when scrolling through pictures to remind you of people and times. One of the least heard regrets is that we should have taken more pictures. The number one tip for having a great first time home buying experience is to

The number one tip for having a great first time home buying experience is to

Granite counter-tops are all the rage and it seems that everyone is putting these in their homes these days. A good thing about granite counter-tops is that it is very hard to damage them. Granite counter-tops are basically fool proof. They will cost you around 2,000-6,000 but are well worth the money. The only con I can think of when it comes to granite counter-tops is that you may need to reseal them every now and again because the edges and corners can chip. This will need to be done by a professional.

Granite counter-tops are all the rage and it seems that everyone is putting these in their homes these days. A good thing about granite counter-tops is that it is very hard to damage them. Granite counter-tops are basically fool proof. They will cost you around 2,000-6,000 but are well worth the money. The only con I can think of when it comes to granite counter-tops is that you may need to reseal them every now and again because the edges and corners can chip. This will need to be done by a professional.  "If you are in the market to buy a home, today's average mortgage rates are something to celebrate compared to almost any year since 1971.

"If you are in the market to buy a home, today's average mortgage rates are something to celebrate compared to almost any year since 1971.