Do You Have Enough Homeowners Insurance?

The news lately has been filled with reports of tornadoes, hurricanes, floods, and fires, each of which has resulted in untold loss of lives, homes, and possessions. As we watch with horror the impact these disasters have on those  affected, it is only natural that we ask ourselves,” Would I be able to sustain such losses? Would my homeowners insurance policy cover the costs of rebuilding my home?

affected, it is only natural that we ask ourselves,” Would I be able to sustain such losses? Would my homeowners insurance policy cover the costs of rebuilding my home?

The National Association of Insurance Commissioners (NAIC)) recommends that you use your annual renewal notice or any improvements to your home as a reminder to touch base with your agent or insurer to recheck how much insurance you really need. Do you have sufficient coverage for rebuilding and replacement? Amy Bach, executive director of United Policyholders, a consumer advocacy group, urges homeowners not to blindly trust that their home insurer has all the bases covered.

With fluctuations in the real estate market, coverage equal to the current replacement cost (excluding land), is advisable. The first step in getting adequate coverage is to establish your policy’s dwelling limit. Your target number is the full-replacement cost of your home and its possessions. The dwelling limit bears no relation to your property’s market value, its appraised value, or its assessed tax value. And don’t mistake the cost of new construction for the cost to rebuild, which is more expensive because of factors such as debris removal and higher demand for materials and labor after a catastrophe,

(You can get a pretty good idea of what it would cost to rebuild your home by using an online calculator, available at sites such as HMFacts.com ($7) and AccuCoverage.com ($8).

It’s a good idea to purchase guaranteed replacement coverage, meaning the insurer will pay whatever it costs to rebuild your home with materials of like kind and quality, without deducting for wear and tear. Avoid actual cash value coverage, which pays only the depreciated value of your home.

Check also on your need for flood insurance, even if you don’t live near a body of water, since policies vary in their coverage of many types of water damage.

And lastly, it goes without saying that you need to update the inventory of your possessions at least annually since it is not only a record of the contents of your house and their value, but also a good indicator of whether you have enough coverage.

Information courtesy of Montgomery AL Realtor Sandra Nickel, Sandra Nickel Hat Team.

Victims of Murphy’s Law can attest that their air conditioner goes out on the hottest day of the year or the water heater fails when you have out of town visitors.

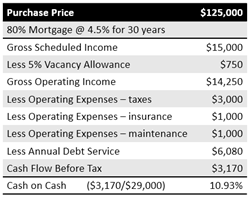

Victims of Murphy’s Law can attest that their air conditioner goes out on the hottest day of the year or the water heater fails when you have out of town visitors. Years ago, real estate investors used to accept negative cash flow buoyed by tax incentives in hopes of making a big payday due to appreciation when they sold it. Today’s investors are focusing on tangible, current results like cash flow and equity build-up.

Years ago, real estate investors used to accept negative cash flow buoyed by tax incentives in hopes of making a big payday due to appreciation when they sold it. Today’s investors are focusing on tangible, current results like cash flow and equity build-up. How old is your bedroom furniture and what did you pay for it? Don’t know? That’s okay, let’s try an easier question. When did you buy the TV in your family room and is it a plasma, LCD or a LED?

How old is your bedroom furniture and what did you pay for it? Don’t know? That’s okay, let’s try an easier question. When did you buy the TV in your family room and is it a plasma, LCD or a LED? Interior updates:

Interior updates: The first assumption that has to be made is that the comparable homes are similar in size, location, condition and amenities. Obviously, a variance in any of these things affects the price per square foot which will not give you a fair comparison.

The first assumption that has to be made is that the comparable homes are similar in size, location, condition and amenities. Obviously, a variance in any of these things affects the price per square foot which will not give you a fair comparison.

ense of community:

ense of community:  More money has been lost to indecision than was ever lost to making the wrong decision. The economy and the housing market have caused some people to take a “wait and see” position that could cost them in lost opportunities as well as almost certain higher costs in the future.

More money has been lost to indecision than was ever lost to making the wrong decision. The economy and the housing market have caused some people to take a “wait and see” position that could cost them in lost opportunities as well as almost certain higher costs in the future.

after all the time and effort you have put into it in previous months. Not to despair, however; it may not be too late to revive—or at least repair---the grassy areas of your landscape. Try following the following steps:

after all the time and effort you have put into it in previous months. Not to despair, however; it may not be too late to revive—or at least repair---the grassy areas of your landscape. Try following the following steps: